Run this tutorial: Open in Colab | Launch Binder

Know your data: datasets and synthetic processes

Start here. Before resampling a series you should know its statistical regime, because that regime is what decides which bootstrap method is valid. Here we load every real dataset and build every synthetic process used elsewhere in the suite, plot each one, name the regime it demonstrates, and preview what diagnose says about it.

The real datasets come from sktime and statsmodels, both pulled in by the tsbootstrap[examples] extra. The synthetic processes are defined inline with nothing but numpy, so the volatility-clustering example needs no financial-data dependency at all.

[1]:

# On Colab or Binder, install tsbootstrap first (skipped if already present):

try:

import tsbootstrap # noqa: F401

except ImportError:

%pip install -q "tsbootstrap[examples]"

Imports

A few imports shared by every cell below.

[2]:

import warnings

import matplotlib.pyplot as plt

import numpy as np

warnings.filterwarnings("ignore") # keep dataset loaders and ADF tests quiet

rng = np.random.default_rng(0)

Bundled real datasets

Six real series, each a different regime. We plot every one and note in a single line what makes it interesting for resampling.

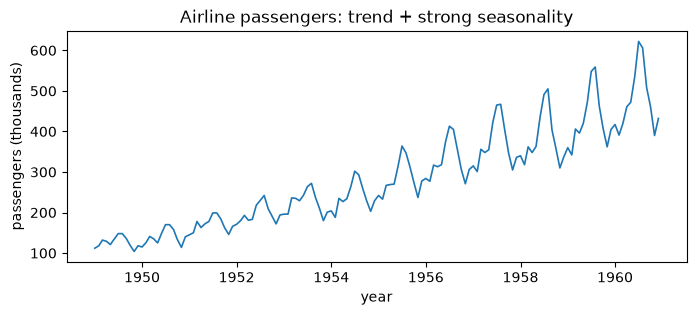

Airline passengers (monthly)

This series has a trend and strong multiplicative seasonality. The dependence is structured, not random, so plain i.i.d. resampling would destroy it.

[3]:

from sktime.datasets import load_airline

airline = load_airline() # pandas Series, PeriodIndex (monthly)

y = airline.to_numpy(dtype=float)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(airline.index.to_timestamp(), y, color="tab:blue", lw=1.2)

ax.set_title("Airline passengers: trend + strong seasonality")

ax.set_xlabel("year")

ax.set_ylabel("passengers (thousands)")

plt.show()

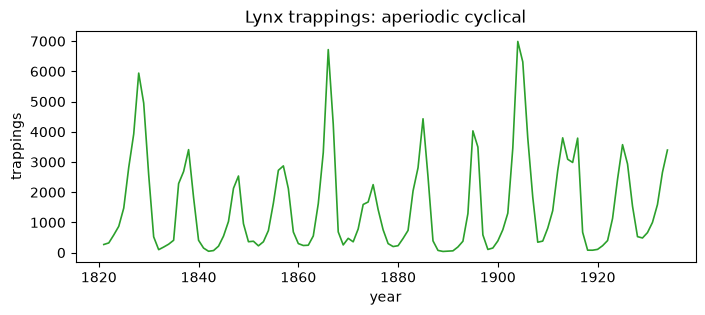

Canadian lynx (annual)

Aperiodic cyclical. The boom-and-bust cycle is real but its period wanders, so it is not clean seasonality.

[4]:

from sktime.datasets import load_lynx

lynx = load_lynx() # pandas Series, PeriodIndex (annual)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(lynx.index.year, lynx.to_numpy(dtype=float), color="tab:green", lw=1.2)

ax.set_title("Lynx trappings: aperiodic cyclical")

ax.set_xlabel("year")

ax.set_ylabel("trappings")

plt.show()

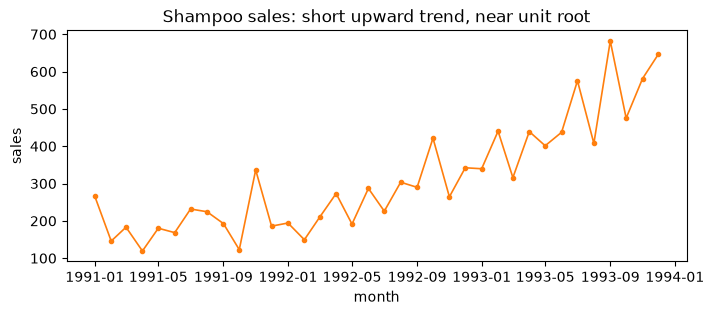

Shampoo sales (monthly)

Short series with an upward trend that sits near a unit root. Only 36 points, so it also stresses methods that assume plenty of data.

[5]:

from sktime.datasets import load_shampoo_sales

shampoo = load_shampoo_sales() # pandas Series, PeriodIndex (monthly), n=36

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(

shampoo.index.to_timestamp(),

shampoo.to_numpy(dtype=float),

color="tab:orange",

lw=1.2,

marker="o",

ms=3,

)

ax.set_title("Shampoo sales: short upward trend, near unit root")

ax.set_xlabel("month")

ax.set_ylabel("sales")

plt.show()

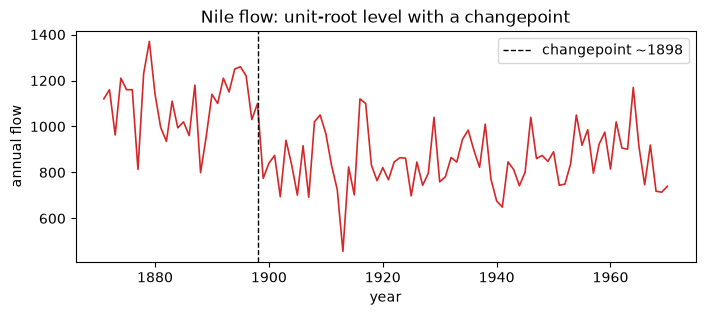

Nile river flow (annual)

A unit-root level with a well-known changepoint near 1898 (construction of the Aswan dam reduced the flow). A clear case where the series is non-stationary.

[6]:

from statsmodels.datasets import nile

nile_df = nile.load_pandas().data # columns: year, volume

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(nile_df["year"], nile_df["volume"], color="tab:red", lw=1.2)

ax.axvline(1898, color="black", ls="--", lw=1.0, label="changepoint ~1898")

ax.set_title("Nile flow: unit-root level with a changepoint")

ax.set_xlabel("year")

ax.set_ylabel("annual flow")

ax.legend()

plt.show()

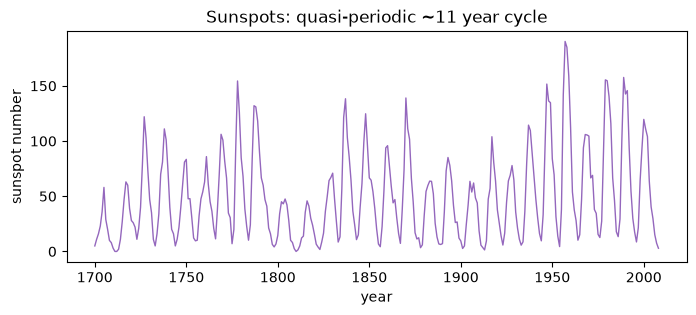

Sunspots (yearly)

Quasi-periodic, with a roughly 11 year solar cycle whose amplitude varies. A good test for methods that must preserve a dominant but inexact cycle.

[7]:

from statsmodels.datasets import sunspots

sun_df = sunspots.load_pandas().data # columns: YEAR, SUNACTIVITY

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(sun_df["YEAR"], sun_df["SUNACTIVITY"], color="tab:purple", lw=1.0)

ax.set_title("Sunspots: quasi-periodic ~11 year cycle")

ax.set_xlabel("year")

ax.set_ylabel("sunspot number")

plt.show()

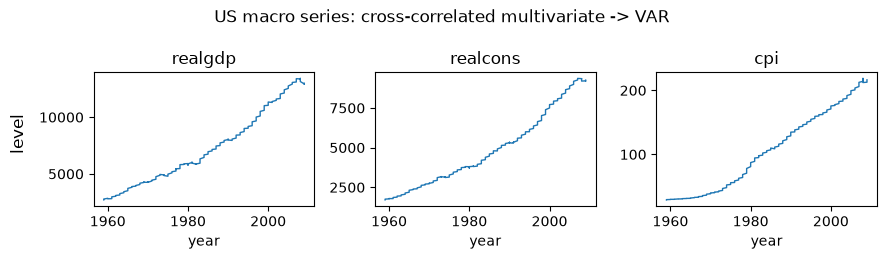

US macro indicators (quarterly, multivariate)

Three cross-correlated series: real GDP, real consumption, and the CPI. The cross-series dependence is the point: this is the regime where a VAR model, which captures how the series move together, is the natural choice.

[8]:

from statsmodels.datasets import macrodata

macro_df = macrodata.load_pandas().data

cols = ["realgdp", "realcons", "cpi"]

macro = macro_df[cols].to_numpy(dtype=float) # shape (203, 3)

fig, axes = plt.subplots(1, 3, figsize=(9, 2.6), sharex=True)

for ax, col in zip(axes, cols):

ax.plot(macro_df["year"], macro_df[col], lw=1.0)

ax.set_title(col)

ax.set_xlabel("year")

fig.supylabel("level")

fig.suptitle("US macro series: cross-correlated multivariate -> VAR")

fig.tight_layout()

plt.show()

Synthetic data-generating processes

Now the controlled cases. Because we define each process, we know its true properties exactly, which makes them ideal for checking that a method recovers what it should. Everything below is plain numpy.

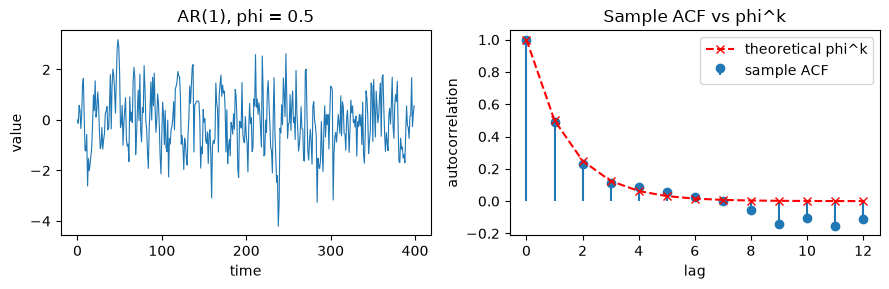

AR(1), phi = 0.5: known theoretical ACF

For a stationary AR(1) the autocorrelation at lag k is exactly rho_k = phi^k. We overlay the sample ACF against that closed form to confirm the match.

[9]:

def ar1(n, phi, rng):

x = np.zeros(n)

e = rng.standard_normal(n)

for t in range(1, n):

x[t] = phi * x[t - 1] + e[t]

return x

def sample_acf(x, max_lag):

x = x - x.mean()

denom = np.dot(x, x)

return np.array(

[np.dot(x[: -k or None], x[k:]) / denom if k else 1.0 for k in range(max_lag + 1)]

)

phi = 0.5

x_ar1 = ar1(400, phi, rng)

max_lag = 12

acf_hat = sample_acf(x_ar1, max_lag)

acf_true = phi ** np.arange(max_lag + 1)

fig, (a1, a2) = plt.subplots(1, 2, figsize=(9, 3))

a1.plot(x_ar1, color="tab:blue", lw=0.8)

a1.set_title("AR(1), phi = 0.5")

a1.set_xlabel("time")

a1.set_ylabel("value")

lags = np.arange(max_lag + 1)

a2.stem(lags, acf_hat, linefmt="tab:blue", markerfmt="o", basefmt=" ", label="sample ACF")

a2.plot(lags, acf_true, "r--", marker="x", label="theoretical phi^k")

a2.set_title("Sample ACF vs phi^k")

a2.set_xlabel("lag")

a2.set_ylabel("autocorrelation")

a2.legend()

fig.tight_layout()

plt.show()

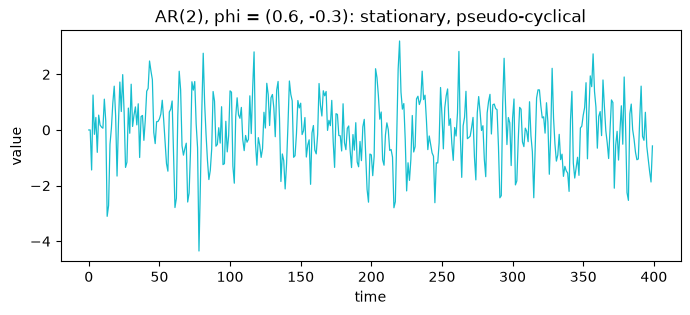

AR(2)

A second-order process can produce pseudo-cyclical behavior from pure linear dynamics, with no seasonal term involved.

[10]:

def ar2(n, phi1, phi2, rng):

x = np.zeros(n)

e = rng.standard_normal(n)

for t in range(2, n):

x[t] = phi1 * x[t - 1] + phi2 * x[t - 2] + e[t]

return x

x_ar2 = ar2(400, 0.6, -0.3, rng)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(x_ar2, color="tab:cyan", lw=0.9)

ax.set_title("AR(2), phi = (0.6, -0.3): stationary, pseudo-cyclical")

ax.set_xlabel("time")

ax.set_ylabel("value")

plt.show()

Seasonal plus trend

A deterministic linear trend with a sine seasonal component and additive noise. The non-stationary mean comes entirely from the trend term.

[11]:

n = 400

t = np.arange(n)

period = 24

x_seas = 0.02 * t + 2.0 * np.sin(2 * np.pi * t / period) + rng.standard_normal(n)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(t, x_seas, color="tab:olive", lw=0.9)

ax.set_title("Trend + seasonal: deterministic non-stationary mean")

ax.set_xlabel("time")

ax.set_ylabel("value")

plt.show()

Random walk: unit root

This is the textbook non-stationary process. Its variance grows without bound, so any method that assumes a fixed level will misrepresent it.

[12]:

x_rw = np.cumsum(rng.standard_normal(400))

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(x_rw, color="tab:brown", lw=0.9)

ax.set_title("Random walk: unit root (non-stationary)")

ax.set_xlabel("time")

ax.set_ylabel("value")

plt.show()

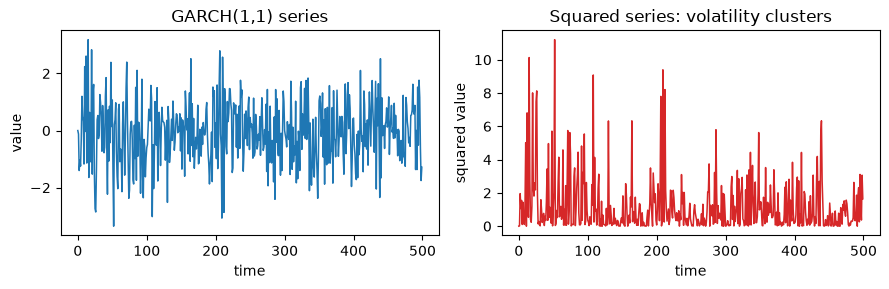

GARCH(1,1): volatility clustering, no financial data

This is how the suite demonstrates volatility clustering without any market data. We simulate the conditional variance recursion sigma2_t = omega + alpha * e_{t-1}^2 + beta * sigma2_{t-1} and draw e_t = sigma_t * z_t. Plotting the squared series makes the clustering obvious: large moves bunch together in time.

[13]:

def garch11(n, omega, alpha, beta, rng):

e = np.zeros(n)

sigma2 = np.empty(n)

sigma2[0] = omega / (1 - alpha - beta) # unconditional variance

z = rng.standard_normal(n)

for t in range(1, n):

sigma2[t] = omega + alpha * e[t - 1] ** 2 + beta * sigma2[t - 1]

e[t] = np.sqrt(sigma2[t]) * z[t]

return e

x_garch = garch11(500, omega=0.05, alpha=0.1, beta=0.85, rng=rng)

fig, (g1, g2) = plt.subplots(1, 2, figsize=(9, 3))

g1.plot(x_garch, color="tab:blue", lw=1.1)

g1.set_title("GARCH(1,1) series")

g1.set_xlabel("time")

g1.set_ylabel("value")

g2.plot(x_garch**2, color="tab:red", lw=1.1)

g2.set_title("Squared series: volatility clusters")

g2.set_xlabel("time")

g2.set_ylabel("squared value")

fig.tight_layout()

plt.show()

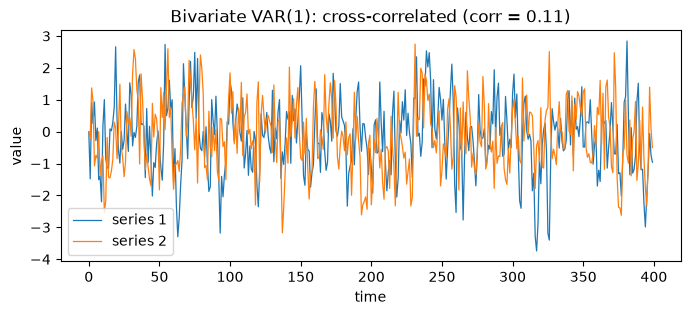

Bivariate VAR(1): cross-correlated 2D

Two series whose dynamics are coupled through a coefficient matrix. The off diagonal terms make each series depend on the other’s past, which is exactly the structure a VAR-based bootstrap is built to preserve.

[14]:

def var1(n, A, rng):

d = A.shape[0]

X = np.zeros((n, d))

E = rng.standard_normal((n, d))

for t in range(1, n):

X[t] = A @ X[t - 1] + E[t]

return X

A = np.array([[0.5, 0.2], [0.1, 0.4]])

X_var = var1(400, A, rng)

fig, ax = plt.subplots(figsize=(8, 3))

ax.plot(X_var[:, 0], color="tab:blue", lw=0.9, label="series 1")

ax.plot(X_var[:, 1], color="tab:orange", lw=0.9, label="series 2")

corr = np.corrcoef(X_var[:, 0], X_var[:, 1])[0, 1]

ax.set_title(f"Bivariate VAR(1): cross-correlated (corr = {corr:.2f})")

ax.set_xlabel("time")

ax.set_ylabel("value")

ax.legend()

plt.show()

A diagnose() preview

diagnose measures serial dependence and stationarity, then maps what it sees to method specifications. It returns a Diagnosis dataclass; the two fields we read here are recommended_methods and notes. We run it across a representative mix of the series above.

diagnose reports what it measures and maps it to candidate methods. The decision-guide notebook works through when each recommended method is the right choice.

[15]:

from tsbootstrap import diagnose

probes = {

"AR(1) stationary": x_ar1,

"random walk": x_rw,

"airline (trend+seasonal)": y,

"GARCH(1,1)": x_garch,

"VAR(1) bivariate": X_var,

}

for name, series in probes.items():

d = diagnose(series)

print(f"{name}:")

print(f" recommended_methods: {d.recommended_methods}")

for note in d.notes:

print(f" note: {note}")

print()

AR(1) stationary:

recommended_methods: ('StationaryBlock', 'MovingBlock', 'SieveAR')

note: Serial dependence present (lag-1 autocorrelation 0.49): use a block method or the sieve.

note: Suggested automatic block length (Politis-White): 9.

random walk:

recommended_methods: ('ResidualBootstrap(model=ARIMA(...))', 'SieveAR')

note: Series looks non-stationary (unit root): difference it via ARIMA, or use the sieve.

airline (trend+seasonal):

recommended_methods: ('ResidualBootstrap(model=ARIMA(...))', 'SieveAR')

note: Series looks non-stationary (unit root): difference it via ARIMA, or use the sieve.

GARCH(1,1):

recommended_methods: ('IID', 'MovingBlock')

note: Serial dependence is weak: i.i.d. resampling is acceptable; a block method is a safe default.

VAR(1) bivariate:

recommended_methods: ('ResidualBootstrap(model=VAR(...))', 'StationaryBlock', 'MovingBlock', 'SieveAR')

note: Serial dependence present (lag-1 autocorrelation 0.48): use a block method or the sieve.

note: Multivariate input: VAR captures cross-series dependence; block methods preserve it by resampling whole rows.

note: Suggested automatic block length (Politis-White): 7.