Run this tutorial: Open in Colab | Launch Binder

Quickstart: your first bootstrap

tsbootstrap resamples time series. The whole public API is one function, bootstrap, configured with a typed method specification. To get going we run a block bootstrap, read its results, and ask diagnose which method fits the data.

[1]:

# On Colab or Binder, install tsbootstrap first (skipped if already present):

try:

import tsbootstrap # noqa: F401

except ImportError:

%pip install -q "tsbootstrap[examples]"

A small series

We use a stationary AR(1) process so the dependence structure is known.

[2]:

import numpy as np

rng = np.random.default_rng(0)

n, phi = 200, 0.6

x = np.zeros(n)

for t in range(1, n):

x[t] = phi * x[t - 1] + rng.standard_normal()

x[:5]

[2]:

array([ 0. , 0.12573022, -0.05666673, 0.60642261, 0.46875368])

One bootstrap call

MovingBlock(block_length="auto") picks the block length with the Politis-White rule. The result carries the samples plus provenance and out-of-bag primitives.

[3]:

from tsbootstrap import MovingBlock, bootstrap

result = bootstrap(x, method=MovingBlock(block_length="auto"), n_bootstraps=200, random_state=0)

samples = result.values()

samples.shape # (n_bootstraps, n)

[3]:

(200, 200)

Going faster (optional)

For larger runs, bootstrap accepts backend="compiled", an opt-in numba-accelerated fast path. It is equal in distribution to the default numpy path but not bit-identical, so individual replicates differ even with the same random_state. It needs the extra dependency, installed with pip install "tsbootstrap[accel]".

result_fast = bootstrap(x, method=MovingBlock(block_length="auto"), n_bootstraps=200, random_state=0, backend="compiled")

Out-of-bag mask

Observation-resampling methods record which points were left out of each replicate. This out-of-bag structure is what the EnbPI uncertainty layer builds on.

[4]:

mask = result.get_oob_mask()

mask.shape, round(float(mask.mean()), 3) # ~0.37 of points are OOB per replicate

[4]:

((200, 200), 0.361)

Which method should I use?

diagnose inspects the series (serial dependence, stationarity) and recommends method specifications. It is a heuristic starting point, not a guarantee; the decision-guide tutorial shows when each method is the right choice.

[5]:

from tsbootstrap import diagnose

diagnose(x).recommended_methods

[5]:

('StationaryBlock', 'MovingBlock', 'SieveAR')

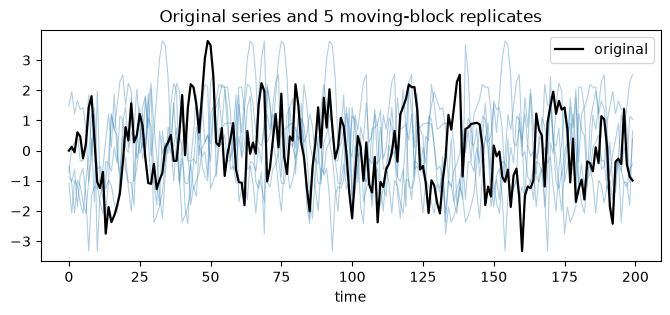

Visualizing replicates

Each replicate is a new series that preserves the local dependence of the original.

[6]:

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(8, 3))

for i in range(5):

ax.plot(samples[i], color="tab:blue", alpha=0.35, lw=0.8)

ax.plot(x, color="black", lw=1.6, label="original")

ax.set_title("Original series and 5 moving-block replicates")

ax.set_xlabel("time")

ax.legend()

plt.show()

A confidence interval in one call

Beyond resampled series, conf_int gives a confidence interval for a statistic of the series in one call: it runs the bootstrap and reads back the interval. The call below returns a bias-corrected and accelerated (BCa) interval for the mean.

[7]:

from tsbootstrap import IID, conf_int

lower, upper, point = conf_int(x, "mean", method=IID(), kind="bca", alpha=0.1)

print(f"90% BCa interval for the mean: [{float(lower):.3f}, {float(upper):.3f}]")

90% BCa interval for the mean: [-0.099, 0.182]