Run this tutorial: Open in Colab | Launch Binder

Classical confidence intervals in one call

conf_int turns a bootstrap run into a confidence interval for a statistic of one series. You pass the series, the statistic, and a method spec; it runs the bootstrap and reads back the interval you asked for. This tour builds percentile, basic, and studentized intervals on a dependent AR(1) series, shows why BCa is refused for block methods (and why that refusal protects you), and finishes with per-series intervals over a ragged panel.

The four interval families, shortest to say:

percentileandbasicare first-order correct and need only the replicate distribution.studentizedis second-order correct for smooth statistics when its per-replicate standard error is dependence-aware, whichconf_intarranges with a block jackknife.bcacorrects for bias and skewness, but its acceleration is defined under independent sampling, so it is offered for theIIDspec only.

Coverage here is approximate or asymptotic under temporal dependence, not finite-sample distribution-free, the same honest ceiling as the rest of the uq layer.

[1]:

# On Colab or Binder, install tsbootstrap first (skipped if already present):

try:

import tsbootstrap # noqa: F401

except ImportError:

%pip install -q "tsbootstrap[examples]"

A dependent series

We use an AR(1) series with positive autocorrelation and a true mean of zero. The dependence is what makes the interval choice matter: a naive i.i.d. interval would understate the variance of the sample mean, so it would be too narrow.

[2]:

import numpy as np

def ar1(phi, n, seed):

"""AR(1) started at its first innovation; true mean 0 for zero drift."""

rng = np.random.default_rng(seed)

e = rng.standard_normal(n)

x = np.empty(n)

x[0] = e[0]

for t in range(1, n):

x[t] = phi * x[t - 1] + e[t]

return x

x = ar1(0.5, 200, seed=0)

print(f"series length {x.size}, sample mean {x.mean():.3f}")

series length 200, sample mean 0.030

Percentile, basic, and studentized, one call each

Each interval is a single conf_int call. We use a MovingBlock method so the resampling respects the AR(1) dependence, a small n_bootstraps to keep the tutorial quick, and the built-in "mean" statistic. The studentized path estimates a dependence-aware standard error with a block jackknife on its own; you do not have to supply one.

[3]:

from tsbootstrap import MovingBlock, conf_int

ALPHA = 0.1 # 90% intervals

B = 399

method = MovingBlock(block_length="auto")

intervals = {}

point = None

for kind in ("percentile", "basic", "studentized"):

lower, upper, point = conf_int(

x, "mean", method=method, kind=kind, alpha=ALPHA, n_bootstraps=B, random_state=0

)

intervals[kind] = (float(lower), float(upper))

print(f"point estimate (sample mean): {float(point):.3f}")

point estimate (sample mean): 0.030

[4]:

import pandas as pd

summary = pd.DataFrame(

{

kind: {

"lower": lo,

"upper": hi,

"width": hi - lo,

"covers 0": "yes" if lo <= 0.0 <= hi else "no",

}

for kind, (lo, hi) in intervals.items()

}

).T

summary.round(4)

[4]:

| lower | upper | width | covers 0 | |

|---|---|---|---|---|

| percentile | -0.190865 | 0.301442 | 0.492307 | yes |

| basic | -0.241749 | 0.250558 | 0.492307 | yes |

| studentized | -0.24268 | 0.283117 | 0.525797 | yes |

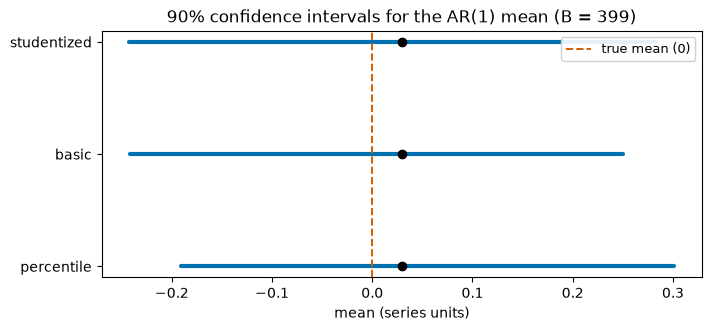

All three intervals bracket the true mean of zero. The percentile and basic bands have the same width because basic is the percentile band reflected through the point estimate. The studentized band is a little wider: it accounts for the extra uncertainty in the per-replicate standard error, which is the cost of its second-order correctness under dependence.

A picture of the three intervals

The same three intervals drawn as error bars around the point estimate, with the true mean marked.

[5]:

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(7, 3.2), layout="constrained")

names = list(intervals)

for i, (lo, hi) in enumerate(intervals.values()):

ax.plot([lo, hi], [i, i], color="#0072B2", lw=3, solid_capstyle="round")

ax.plot(float(point), i, marker="o", color="black", zorder=5)

ax.axvline(0.0, color="#D55E00", ls="--", lw=1.4, label="true mean (0)")

ax.set_yticks(range(len(names)))

ax.set_yticklabels(names)

ax.set_xlabel("mean (series units)")

ax.set_title(f"90% confidence intervals for the AR(1) mean (B = {B})")

ax.legend(loc="upper right", fontsize=9, framealpha=0.9)

plt.show()

Why BCa is refused for block methods

BCa corrects the percentile interval for median bias and skewness, which makes it a strong default on i.i.d. data. Its acceleration constant, though, is a delete-one jackknife estimate that is only defined under independent sampling (Efron 1987). There is no valid drop-in version of that constant for dependent data, so asking for kind="bca" with a block method raises a typed error rather than quietly returning an interval built on an invalid constant. The refusal is doing its job: it

protects the statistical validity of the result and points you at the studentized interval, which is the second-order-correct route for dependent data.

[6]:

from tsbootstrap.errors import MethodConfigError

try:

conf_int(x, "mean", method=MovingBlock(block_length="auto"), kind="bca", alpha=ALPHA)

except MethodConfigError as exc:

print("MethodConfigError raised, as intended:\n")

print(exc)

MethodConfigError raised, as intended:

[TSB_UNSUPPORTED_MODEL_FEATURE] BCa intervals are only supported with the IID method spec; got MovingBlock. The acceleration constant is a delete-one jackknife estimate defined under independent observations (Efron 1987); for dependent data the second-order-correct route is the studentized interval (Gotze and Kunsch 1996). Hint: Use kind='studentized' or kind='percentile' with this method, or method=IID() when the observations are exchangeable.

BCa on i.i.d. data, where it belongs

With the IID spec the acceleration is well defined, so BCa runs and returns a skew-corrected interval. On a right-skewed statistic this is where BCa earns its keep over the plain percentile band: both bands bracket the true mean of 1, but the BCa band shifts to correct the skew.

[7]:

from tsbootstrap import IID

skewed = np.random.default_rng(1).exponential(1.0, size=60) # true mean 1, right-skewed

lo_pct, hi_pct, _ = conf_int(

skewed, "mean", method=IID(), kind="percentile", alpha=ALPHA, n_bootstraps=999, random_state=1

)

lo_bca, hi_bca, _ = conf_int(

skewed, "mean", method=IID(), kind="bca", alpha=ALPHA, n_bootstraps=999, random_state=1

)

print(f"sample mean: {skewed.mean():.3f}")

print(f"percentile: [{lo_pct:.3f}, {hi_pct:.3f}]")

print(f"BCa: [{lo_bca:.3f}, {hi_bca:.3f}] (shifted right to correct the skew)")

sample mean: 1.116

percentile: [0.851, 1.432]

BCa: [0.865, 1.473] (shifted right to correct the skew)

Intervals over a ragged panel

conf_int_panel computes a per-series interval for a whole collection of series in one pass, even when they have different lengths. It builds on the panel bootstrap, so it takes the observation-resampling methods only. The studentized panel path needs an explicit block length: a replicate reducer sees one series at a time without its identity, so a per-series automatic block length cannot be resolved honestly. We pass se_block_length to supply it.

[8]:

from tsbootstrap import conf_int_panel

panel = [ar1(0.4, n, seed=100 + i) for i, n in enumerate((120, 180, 90))]

lower, upper, point = conf_int_panel(

panel,

"mean",

method=MovingBlock(block_length=10),

kind="studentized",

alpha=ALPHA,

se_block_length=10,

n_bootstraps=299,

random_state=0,

)

panel_table = pd.DataFrame(

{"length": [s.size for s in panel], "point": point, "lower": lower, "upper": upper}

)

panel_table.index.name = "series"

panel_table.round(4)

[8]:

| length | point | lower | upper | |

|---|---|---|---|---|

| series | ||||

| 0 | 120 | 0.1328 | -0.0270 | 0.3817 |

| 1 | 180 | -0.1221 | -0.2695 | 0.0518 |

| 2 | 90 | -0.0530 | -0.3899 | 0.2961 |

When to use which

Reach for

percentileorbasicas the distribution-free default; they assume the least and work with every method.Use

studentizedwhen you want second-order accuracy under dependence and can afford the block-jackknife standard error. It is the recommended route for time series.Use

bcafor i.i.d. data with a skewed statistic, where its bias and skew correction buys real accuracy.conf_intrefuses it for dependent methods rather than return a constant that is not valid there.Use

conf_int_panelwhen you have many series and want an interval for each in one pass.

Whatever the family, the coverage claim stays approximate or asymptotic under temporal dependence, so read these as calibrated guidance rather than exact guarantees.