Run this tutorial: Open in Colab | Launch Binder

Cheat sheet: pick your bootstrap

A scannable reference for choosing a tsbootstrap method. The capability table below is built from the library’s own metadata, so it cannot drift from the code. The decision tree summarizes when each family applies.

For the programmatic version of this table, see diagnose, which inspects your data and recommends methods. For the worked rationale behind each choice, see the which-bootstrap-when tutorial.

[1]:

# On Colab or Binder, install tsbootstrap first (skipped if already present):

try:

import tsbootstrap # noqa: F401

except ImportError:

%pip install -q "tsbootstrap[examples]"

The capability table

One row per method, read straight from tsbootstrap.metadata.METHODS and the spec classes in tsbootstrap.methods. The block-length column reports the actual parameter name on each spec (most use block_length; the stationary bootstrap uses avg_block_length; model-based methods have none).

[2]:

import pandas as pd

from tsbootstrap.metadata import METHODS

from tsbootstrap.methods import OBSERVATION_RESAMPLING

def block_length_param(spec_type):

"""Return the block-length field name on a spec, or None if it has none."""

fields = getattr(spec_type, "model_fields", {})

for name in fields:

if "block_length" in name:

return name

return None

def recommended_for(meta, is_resampler):

"""Distill a one-line use case from assumptions and failure modes."""

if not meta.preserves_temporal_dependence:

return "i.i.d. data with no serial dependence; baseline"

if is_resampler:

return "stationary, weakly dependent series; distribution-free"

return "series well described by a fitted AR/ARIMA/VAR model"

rows = []

for spec_type, meta in METHODS.items():

is_resampler = spec_type in OBSERVATION_RESAMPLING

# Resamplers reuse observed values, so they preserve the empirical marginal.

# Model-based methods regenerate from fitted dynamics, so their marginal is

# model-implied rather than empirical.

marginal = "empirical" if is_resampler else "model-implied"

rows.append(

{

"method": meta.name,

"spec": spec_type.__name__,

"serial dependence": "yes" if meta.preserves_temporal_dependence else "no",

"marginal": marginal,

"block-length param": block_length_param(spec_type) or "none",

"wraps around": "yes" if spec_type.__name__ == "CircularBlock" else "no",

"multivariate": "yes" if meta.supports_multivariate else "no",

"OOB": "yes" if meta.supports_oob else "no",

"recommended for": recommended_for(meta, is_resampler),

}

)

table = pd.DataFrame(rows).set_index("method")

table

[2]:

| spec | serial dependence | marginal | block-length param | wraps around | multivariate | OOB | recommended for | |

|---|---|---|---|---|---|---|---|---|

| method | ||||||||

| iid | IID | no | empirical | none | no | yes | yes | i.i.d. data with no serial dependence; baseline |

| moving_block | MovingBlock | yes | empirical | block_length | no | yes | yes | stationary, weakly dependent series; distribut... |

| circular_block | CircularBlock | yes | empirical | block_length | yes | yes | yes | stationary, weakly dependent series; distribut... |

| stationary_block | StationaryBlock | yes | empirical | avg_block_length | no | yes | yes | stationary, weakly dependent series; distribut... |

| non_overlapping_block | NonOverlappingBlock | yes | empirical | block_length | no | yes | yes | stationary, weakly dependent series; distribut... |

| tapered_block | TaperedBlock | yes | empirical | block_length | no | yes | yes | stationary, weakly dependent series; distribut... |

| residual | ResidualBootstrap | yes | model-implied | none | no | yes | no | series well described by a fitted AR/ARIMA/VAR... |

| sieve_ar | SieveAR | yes | model-implied | none | no | no | no | series well described by a fitted AR/ARIMA/VAR... |

Reading the columns:

serial dependence: whether the method preserves temporal structure. Only

iiddoes not.marginal: block and i.i.d. methods resample observed values, so the one-dimensional marginal is the empirical one. Model-based methods regenerate data from fitted dynamics, so their marginal is whatever the model implies, not the raw empirical distribution.

block-length param: the constructor argument controlling block size. Pass

"auto"to let the Politis-White rule pick it.wraps around: only

CircularBlockwraps blocks past the series end, which removes the edge bias of plain moving blocks.OOB: whether out-of-bag masks are defined, which the EnbPI uncertainty layer needs.

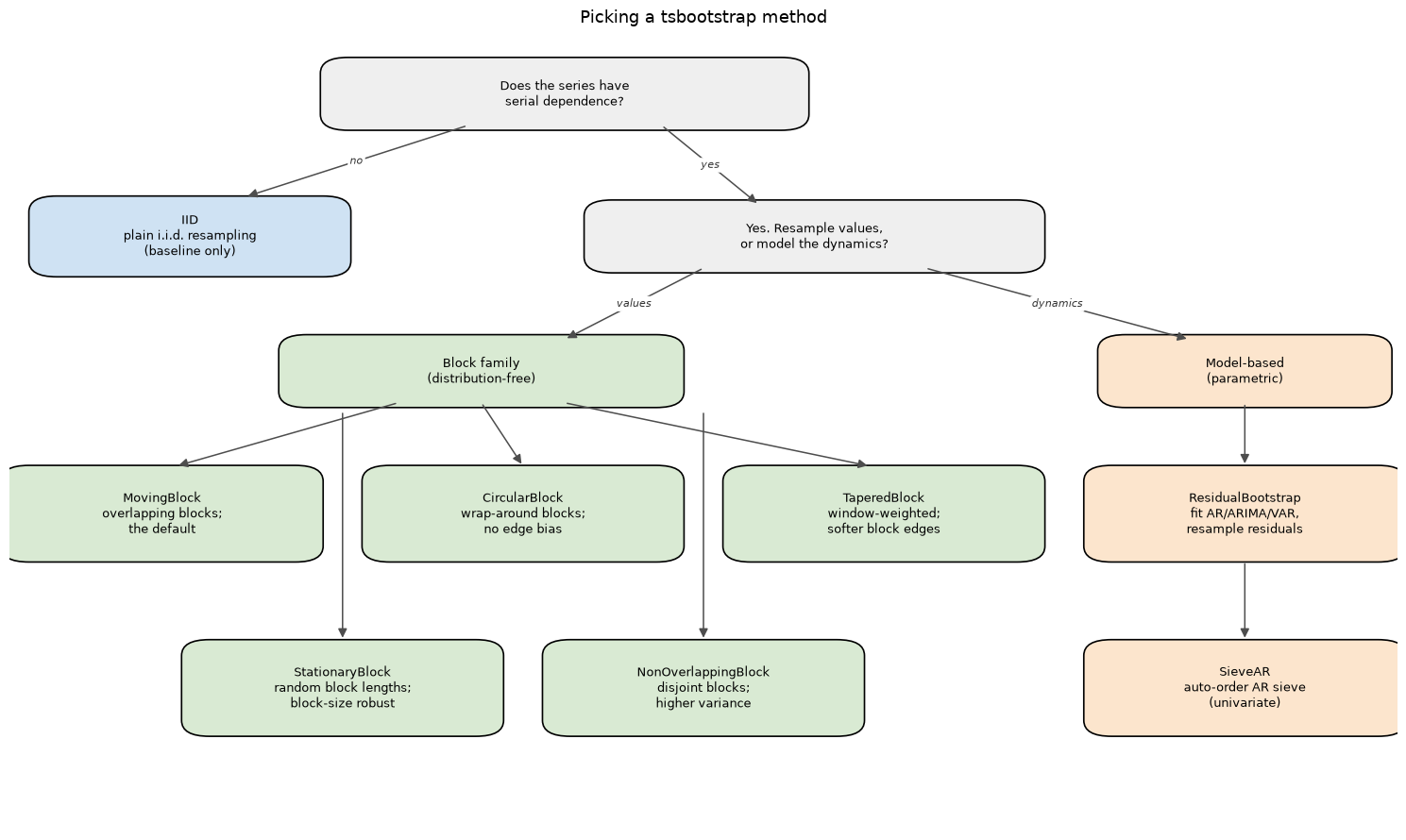

The decision tree

The first split is whether the data has serial dependence. If not, use IID. If it does, choose between a block family (distribution-free, resamples observed values) and a model-based family (regenerates from a fitted model).

[3]:

import matplotlib.pyplot as plt

from matplotlib.patches import FancyArrowPatch, FancyBboxPatch

fig, ax = plt.subplots(figsize=(15, 9))

ax.set_xlim(0, 100)

ax.set_ylim(0, 100)

ax.axis("off")

def box(x, y, w, h, text, color):

"""Draw a rounded box centered text and return its center point."""

patch = FancyBboxPatch(

(x - w / 2, y - h / 2),

w,

h,

boxstyle="round,pad=0.6,rounding_size=2",

linewidth=1.2,

edgecolor="black",

facecolor=color,

)

ax.add_patch(patch)

ax.text(x, y, text, ha="center", va="center", fontsize=9, wrap=True)

return x, y

def arrow(p0, p1, label=None):

"""Draw an arrow from p0 to p1 with an optional mid-label."""

ax.add_patch(

FancyArrowPatch(p0, p1, arrowstyle="-|>", mutation_scale=14, linewidth=1.1, color="0.3")

)

if label:

mx, my = (p0[0] + p1[0]) / 2, (p0[1] + p1[1]) / 2

ax.text(

mx,

my,

label,

ha="center",

va="center",

fontsize=8,

style="italic",

color="0.2",

bbox={"boxstyle": "round,pad=0.2", "fc": "white", "ec": "none"},

)

blue, green, orange, gray = "#cfe2f3", "#d9ead3", "#fce5cd", "#efefef"

# Top level: the first split.

root = box(40, 93, 34, 8, "Does the series have\nserial dependence?", gray)

iid = box(13, 75, 22, 9, "IID\nplain i.i.d. resampling\n(baseline only)", blue)

dep = box(58, 75, 32, 8, "Yes. Resample values,\nor model the dynamics?", gray)

# Second level: the two families, kept far apart on the x-axis.

block = box(34, 58, 28, 8, "Block family\n(distribution-free)", green)

model = box(89, 58, 20, 8, "Model-based\n(parametric)", orange)

# Block family children: a top row of three and a bottom row of two placed in

# the gaps below, all kept clear of the far-right model column.

mb = box(11, 40, 22, 11, "MovingBlock\noverlapping blocks;\nthe default", green)

cb = box(37, 40, 22, 11, "CircularBlock\nwrap-around blocks;\nno edge bias", green)

tb = box(63, 40, 22, 11, "TaperedBlock\nwindow-weighted;\nsofter block edges", green)

sb = box(24, 18, 22, 11, "StationaryBlock\nrandom block lengths;\nblock-size robust", green)

nb = box(50, 18, 22, 11, "NonOverlappingBlock\ndisjoint blocks;\nhigher variance", green)

# Model-based children, stacked in a dedicated far-right column (x = 89).

res = box(89, 40, 22, 11, "ResidualBootstrap\nfit AR/ARIMA/VAR,\nresample residuals", orange)

sv = box(89, 18, 22, 11, "SieveAR\nauto-order AR sieve\n(univariate)", orange)

# Top-level arrows.

arrow((33, 89), (17, 80), "no")

arrow((47, 89), (54, 79), "yes")

arrow((50, 71), (40, 62), "values")

arrow((66, 71), (85, 62), "dynamics")

# Block family to its children. The bottom-row connectors run straight down the

# clear gap columns so they never cross a top-row box.

arrow((28, 54), (12, 46))

arrow((34, 54), (37, 46))

arrow((40, 54), (62, 46))

arrow((24, 53), (24, 24))

arrow((50, 53), (50, 24))

# Model-based family to its children (within the far-right lane).

arrow((89, 54), (89, 46))

arrow((89, 34), (89, 24))

ax.set_title("Picking a tsbootstrap method", fontsize=13, pad=12)

plt.tight_layout()

plt.show()

Confidence intervals in one call

conf_int reads a confidence interval for a statistic straight off a bootstrap run. Pick kind by what you can assume:

percentile/basic: distribution-free default, works with any method.studentized: second-order correct under dependence, works with any method.bca: skew-corrected,IIDspec only.

conf_int_panel does the same per series over a ragged panel.

[4]:

import numpy as np

from tsbootstrap import IID, MovingBlock, conf_int, conf_int_panel

series = np.random.default_rng(0).standard_normal(200)

# Distribution-free percentile interval for the mean, any method:

lo, hi, point = conf_int(

series, "mean", method=MovingBlock(block_length="auto"), kind="percentile", alpha=0.1

)

# Second-order-correct studentized interval under dependence:

lo, hi, point = conf_int(

series, "mean", method=MovingBlock(block_length="auto"), kind="studentized", alpha=0.1

)

# Skew-corrected BCa interval, i.i.d. data only:

lo, hi, point = conf_int(series, "mean", method=IID(), kind="bca", alpha=0.1)

# Per-series intervals over a ragged panel:

panel = [np.random.default_rng(i).standard_normal(n) for i, n in enumerate((120, 180, 90))]

lo, hi, point = conf_int_panel(

panel, "mean", method=MovingBlock(block_length=10), kind="percentile", alpha=0.1

)

print("per-series percentile lower bounds:", np.round(lo, 3))

per-series percentile lower bounds: [-0.109 -0.159 -0.075]

Where to go next

This table and tree are the static reference. Two pointers for using them:

diagnoseis the programmatic version of this table. It inspects your series (serial dependence, stationarity) and returns recommended method specifications. Treat it as a heuristic starting point, not a guarantee:from tsbootstrap import diagnose diagnose(x).recommended_methods

The which-bootstrap-when tutorial walks through the worked rationale: why one family beats another on a given series, and how block length and model order change the answer.